Five years after COVID-19 first swept across the globe, much of sub-Saharan Africa is finding its feet again. Trade volumes have picked up, tourist arrivals are rising, and digital payments have surged.

But for more than 400 million people living in the region’s fragile and conflict-affected states, the promise of recovery is proving elusive.

According to new data from the International Monetary Fund (IMF), more than half of sub-Saharan Africa’s population now lives in states plagued by political instability, armed conflict, or deep institutional fragility.

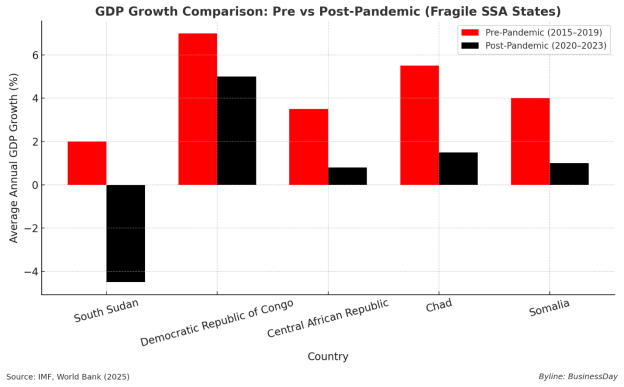

Before the pandemic, fragile states in the region were already lagging behind more stable neighbours. But the economic shock of COVID-19, coupled with ongoing wars, currency depreciation, and weak governance, has widened the gap.

Read also: The Hidden Cost of Logistics: African Inefficiencies and Global Implications

A growing divergence

Before the pandemic, fragile states in the region were already lagging behind more stable neighbours. But the economic shock of COVID-19, coupled with ongoing wars, currency depreciation, and weak governance, has widened the gap.

While non-fragile countries in the region have seen their per capita income recover or even grow since 2020, fragile states remain stuck. IMF estimates show that real per capita income in these countries is still below 2019 levels, even after adjusting for inflation. In some cases, GDP per head has shrunk further.

“More than 70 percent of people suffering from conflict and instability are Africans. Untreated, these conditions become chronic,” said Indermit Gill, Chief Economist at the World Bank.

A June 2025 World Bank brief put it bluntly: fragile countries have experienced a 1.8 percent annual contraction in per capita GDP since the onset of the pandemic, while other low-income countries in Africa have grown by an average of 2.9 percent per year over the same period.

Conflict and capacity

The reasons for this uneven recovery are straightforward but entrenched. Many of these fragile states are either currently in conflict or remain in post-conflict transition. The World Bank lists 21 out of 39 as experiencing high-intensity conflict enough to sap economic productivity and deter investment.

Conflict has devastated agriculture and industry in key areas. In countries like Burkina Faso and Mali, frequent attacks have displaced farmers and reduced food output, driving up prices; these are factors that contributed to military takeovers.

“But the economic shock of COVID-19, coupled with ongoing wars, currency depreciation, and weak governance, has widened the gap.”

In South Sudan, a decade of civil unrest has left critical infrastructure in ruins. Across these states, insecurity has become an economic tax, one that stifles both public and private sector recovery.

But it’s not just violence that holds these economies back. Weak institutions and low state capacity mean even well-intentioned fiscal support or foreign aid often fail to reach those who need it. Budget execution rates are low, tax bases remain narrow, and public trust is limited.

“Jumpstarting growth in fragile states can be done, and it has been done before,” noted M. Ayhan Kose, Deputy Chief Economist at the World Bank. “But it requires sustained political will and tailored international support.”

Read also: Upskilling for the Future: Font Hall and The Future Project empower African youths

Human cost

The economic stagnation in fragile states comes with profound social consequences. The World Bank reports that poverty rates in these countries are double those of their more stable neighbours. Life expectancy is seven years lower, and nearly four in ten children are out of school.

Wenjie Chen, along with co-authors at the IMF, warned in a recent blog that “without a long-term strategy anchored in governance, debt reform, and broad-based development, recovery for fragile states may remain out of reach.”

Across the region, there is concern that without stronger support, these states could fall into a deeper cycle of underdevelopment. Insecurity reduces growth; low growth fuels discontent; discontent breeds instability.

A different kind of recovery

International institutions are calling for a shift in approach. Rather than emergency aid alone, the IMF argues for long-term investments in governance, public finance reform, and economic diversification. There are also calls for greater local engagement, particularly in places where state legitimacy is weak.

The World Bank’s fragile states strategy now emphasises four pillars: conflict prevention, joint security-humanitarian-development action, better governance, and regional partnerships.

“Only a comprehensive approach anchored in country leadership and supported by coordinated international financing can break the pattern,” said Michele Fornino, IMF Africa Department specialist.

But time is short. With debt costs rising, donor fatigue setting in, and political appetite waning, the window for action is narrowing.

Read also: Accra becomes home to Pan-African Progressive Front headquarters

Final thought

Sub-Saharan Africa is not one story; it is many. While some nations are bouncing back, others remain stuck in the pandemic’s long shadow. For fragile states, the challenge is not just economic; it is existential.

If the world wants to see real recovery, then the most vulnerable corners of Africa need more than sympathy. They need solidarity, reform, and a long-term plan.

Oluwatobi Ojabello, senior economic analyst at BusinessDay, holds a BSc and an MSc in Economics as well as a PhD (in view) in Economics (Covenant, Ota).

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp